Australia Targets Digital Asset ATMs with New Task Force

Australia’s financial crimes watchdog, AUSTRAC, is intensifying its efforts against digital asset-related crimes with a new task force dedicated to monitoring cryptocurrency ATMs.

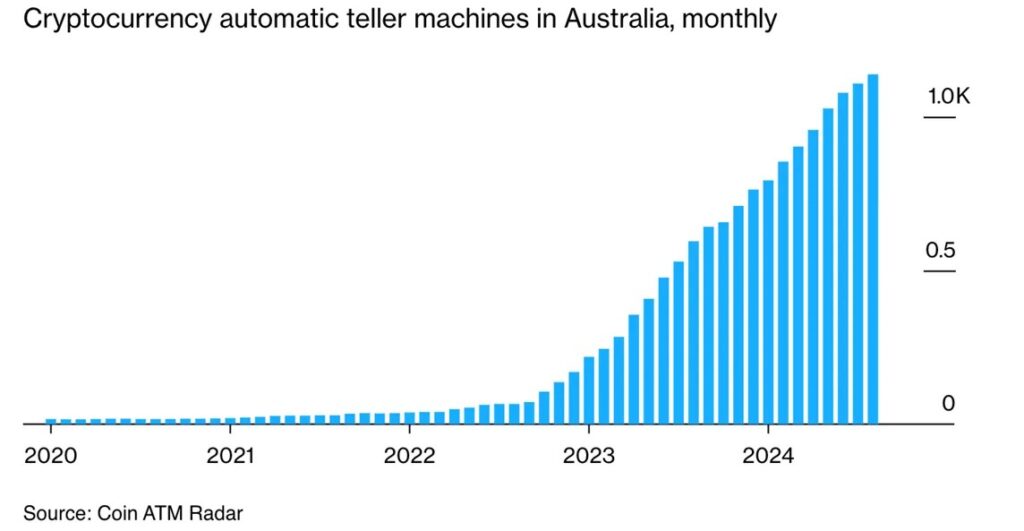

AUSTRAC’s research highlights the growing misuse of digital assets for money laundering and scams. Cryptocurrency ATMs are central to these activities due to their enhanced anonymity, which complicates legal action, and their accessibility—even for Australians with no prior digital asset experience. With 1,323 crypto ATMs, Australia ranks third globally, trailing only the United States and Canada.

The task force will ensure ATM operators comply with AUSTRAC’s strict standards, including robust measures to prevent the machines from being used for illicit purposes. Under Australia’s anti-money laundering (AML) laws, Virtual Asset Service Providers (VASPs), including ATM operators, must monitor transactions, implement Know Your Customer (KYC) protocols, report suspicious activities, and file reports for transactions exceeding AUD10,000 ($6,500).

“Cryptocurrency and crypto ATMs offer criminals a convenient avenue for laundering money due to their accessibility and the ability to conduct instant, irreversible transactions,” said AUSTRAC CEO Brendan Thomas. “As cryptocurrency usage grows, so does its exploitation by criminals, which is why this task force will target non-compliant, high-risk operations.”

Thomas emphasized AUSTRAC’s ongoing commitment to combating crypto-related crimes, making it a key focus for the agency in the coming year.

The use of digital asset ATMs in Australia has surged, climbing from just 100 in 2022 to over 1,300 by 2024. In April 2023, Australia surpassed Asia in the number of cryptocurrency ATMs, surpassing nations like Japan, India, and China. Bitcoin Depot, a leading ATM provider, announced in August that over 200 of its ATMs are pending regulatory approval, signaling continued growth in this space.

AUSTRAC isn’t alone in targeting criminals exploiting cryptocurrency ATMs. Last year, the Australian Federal Police (AFP) identified these machines as a significant tool for scammers and other offenders, citing their widespread availability and the anonymity they provide as key attractions.

However, the surge in ATM numbers isn’t solely driven by criminal activity. According to Chainalysis, only 0.34% of all on-chain transaction volume is linked to illicit activities.

In Australia, a major factor behind the growth of crypto ATMs is the limited access to digital asset on- and off-ramps for retail clients. The country’s largest banks—Commonwealth Bank, Westpac, NAB, and ANZ—have imposed restrictions on fund transfers to and from digital asset exchanges. Together, these banks control over 70% of Australia’s financial market, making alternatives like crypto ATMs essential for users.

US FSOC Raises Alarms Over Stablecoins’ Risk to Financial Stability

In the United States, the Financial Stability Oversight Council (FSOC) has flagged stablecoins as a potential threat to financial stability, citing their vulnerability to sudden runs without proper risk management.

In its latest annual report to Congress, the FSOC highlighted the increasing overlap between digital assets and traditional finance, particularly after the introduction of exchange-traded crypto products in the U.S. However, stablecoins remain the Council’s primary concern due to market concentration and a lack of transparency.

One operator controls 70% of the stablecoin market, with Tether leading at 66% of the $208 billion market through USDT. The FSOC warned that the failure of such a dominant player could destabilize the broader crypto-asset market and have ripple effects on traditional financial systems.

Tether’s dominance has drawn criticism from other regulators as well. The company has faced scrutiny for misleading claims about USDT’s reserves and its financial practices, including being expelled from New York for unlawfully covering up significant financial losses in partnership with Bitfinex.

The FSOC further criticized stablecoin issuers for their lack of transparency, noting that they provide limited, verifiable information about their reserves and management practices.

Janet Yellen, outgoing Treasury Secretary and FSOC chair, urged Congress to establish federal regulations for stablecoin issuers.

“The council continues to call for legislation to create a comprehensive federal prudential framework for stablecoin issuers and to address the risks we have identified in cryptoassets,” she stated.

Post Comment